Global equities generated negative returns over the twelve months to 31 March 2023. Equities suffered a sharp sell-off over the first six months of the period, as geopolitical risk continued to take centre stage, with Russia’s ongoing invasion of Ukraine and central banks’ sharply tightening monetary policy in response to elevated inflationary pressures. Equity markets recouped more than half of the losses over the latter six months of the year though as markets felt confident that a deep recession would be avoided, and investor concerns on tighter monetary policy abated.

In the US, the period ended with Silicon Valley Bank (SVB) entering receivership with the Federal Deposit Insurance Corporation (FDIC) on 10 March 2023, which cited inadequate liquidity and solvency protection.

SVB was the 16th largest bank in the US and represented the largest failure of a bank since the Global Financial Crisis. Shortly after SVB’s demise, investor concerns regarding Credit Suisse accelerated, amidst reports that its top shareholder had ruled out further funding. UBS later agreed to buy Credit Suisse, stabilising the market.

Sterling ended the period 2.6% lower on a trade-weighted basis. Over the course of the year, the Bank of England (BoE) raised its benchmark interest rate cumulatively by 3.5% to 4.25%; and noted that the need for further monetary policy tightening would depend on future evidence concerning the persistence of price pressures. The BoE also became the first major central bank to actively start to unwind quantitative easing, selling £750m of government bonds in November 2022.

Brent crude oil prices fell by 26.1% to $80 per barrel over the twelve months. In Q2 2022, the Organization of the Petroleum Exporting Countries Plus (OPEC+) agreed to a larger-than-expected oil production increase as oil prices surged, increasing production by 648,000 barrels per day during July and August 2022. However, a sharp fall in oil prices in Q3 2022, amid growing fears of recession and weak oil demand from China due to its “zero-covid” policy, prompted OPEC+ to agree to a cut in oil production of 100,000 barrels a day from October. In Q4 2022, OPEC+ agreed to cut production by a further 2 million barrels a day to keep oil prices from falling as a result of weaker global demand, and the period ended with an announcement from the OPEC+ of further surprise oil production cuts of more than 1 million barrels a day.

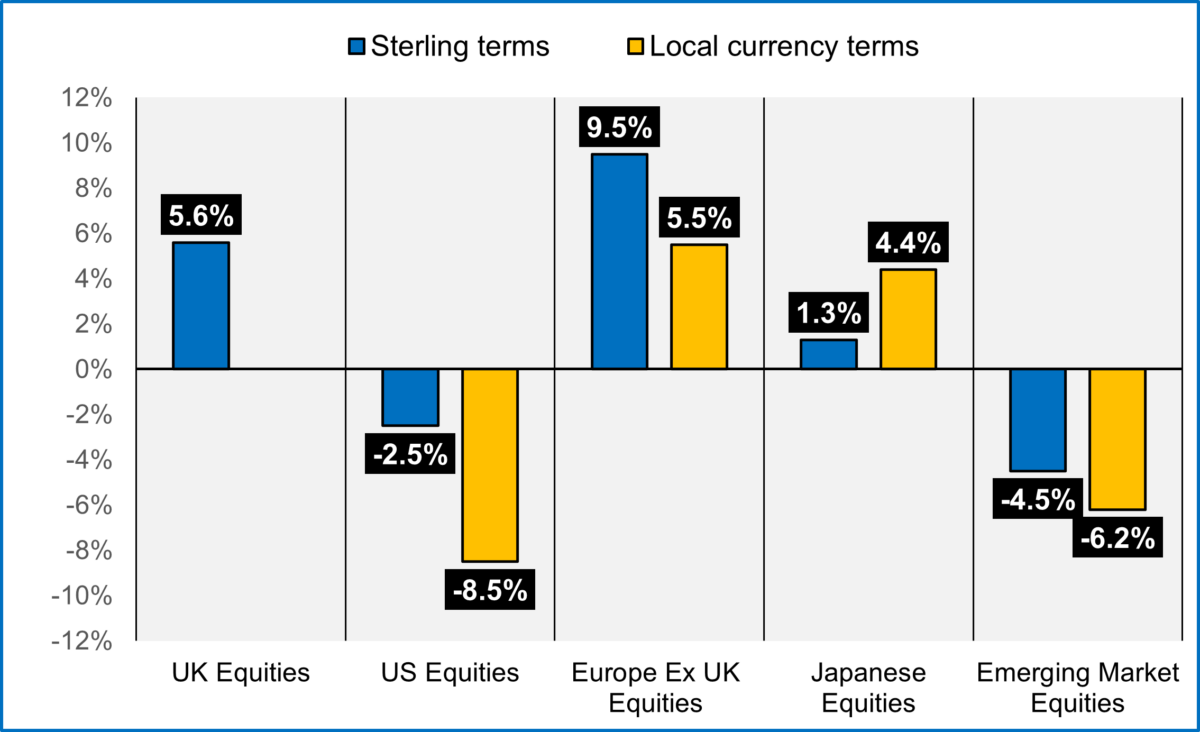

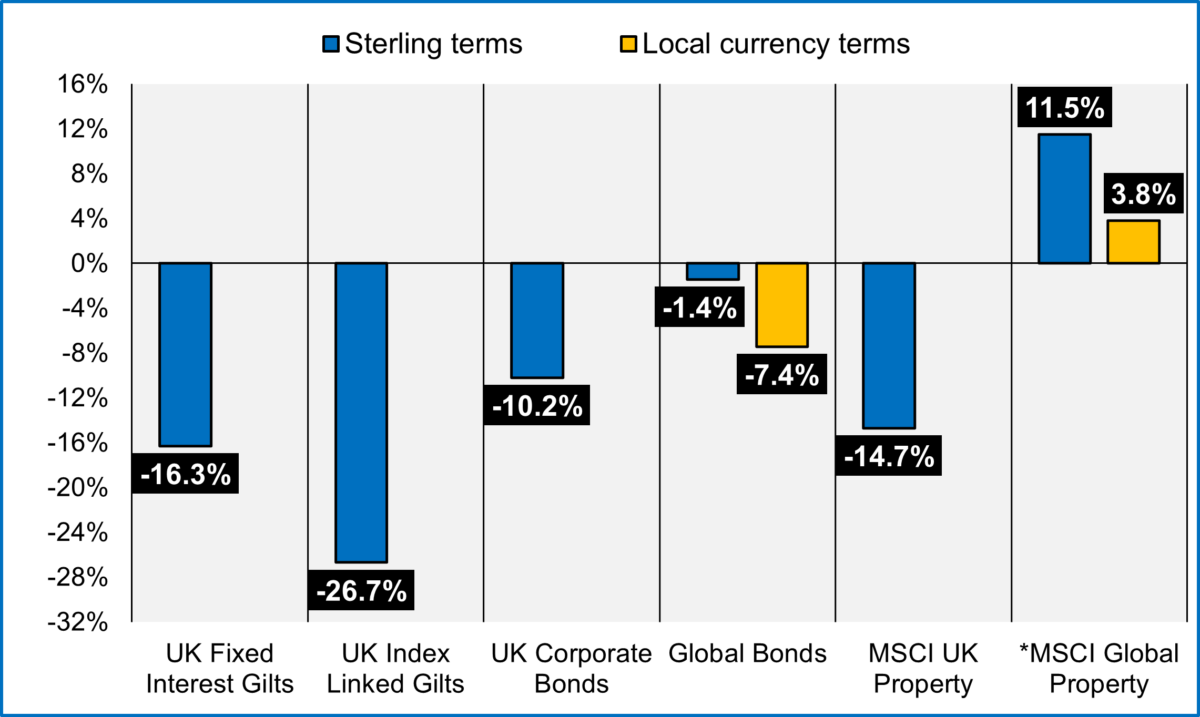

The graphs below summarise the index returns on the main asset classes/regions for the year to 31 March 2023. Returns are shown in sterling terms and local currency terms.

*Global Property returns for 31/12/2021 – 31/12/2022 as annual returns to 31/03/2023 not yet available. Index returns from 31/3/2022 to 31/3/2023. Source: FactSet, MSCI (Equities, Property), FTSE (Gilts), iBoxx (Credit), JP Morgan (Aggregate Global Bonds).

Further details on the performance of specific asset classes over the period are provided below.

Equities

Over the period, US equities were the worst performing equity market, selling off sharply in 2022 as elevated inflation and expectations for higher interest rates weighed on the region; leading to the underperformance of sectors such as Information Technology and Consumer Discretionary. Following SVB’s collapse in March 2023, investors shrugged off short-lived concerns over the banking sector and priced in a quicker end to the sharpest tightening cycle in recent memory. For a major part of 2022, the US dollar exhibited strength due to its status as a safe haven currency, improving returns in sterling terms.

UK equities were the best-performing equity market over the year. Performance was supported by the heavy-weighted Energy sector, which was the best performing sector, as fears over energy supply security grew as a result of the conflict in Ukraine. Economically sensitive sectors such as Industrials and Consumer Discretionary also performed strongly.

European equities were the second-best performing equity market in sterling terms over the period. During Q2 and Q3 2022, performance was poor due to mainland Europe’s close trading relationship with Russia, and in particular, reliance on Russian energy. However, European equities posted strong returns over the next six months, benefiting from falling energy prices and China’s economic reopening.

Japanese equities posted mixed returns in local currency and sterling terms throughout the year, as the Bank of Japan continued to maintain its loose monetary policy in contrast to most central banks. The yen reached a 20-year low against the US dollar during Q2 2022, which the Bank of Japan proceeded to offset in Q3 2022 by selling US dollars for the first-time since 1998. Japanese equities saw positive returns over the second half of the year in line with developed market peers.

Emerging markets were the second worst-performing market over the twelve months. Increases in interest rates by major central banks and a strong dollar resulted in emerging market returns lagging other markets. Brazilian and South Korean equities posted particularly weak returns, whilst Chinese and Indian equities were among the best performers, albeit returns were still negative. Brazil experienced anti-government riots amidst softening economic data, whilst Indian markets are in the midst of allegations of share price manipulation and fraud at a major conglomerate in the country.

UK Fixed Income

UK fixed-interest gilts returned -16.3%, while index-linked gilts returned -26.7% over the year as inflationary concerns drove yields higher. In September 2022, the BoE temporarily announced an emergency £65bn bond-buying programme to stabilise the government debt market, after an unexpected expansionary fiscal package was announced. The package increased investor concern over the sustainability of public finances, resulting in a considerable spike in yields. The sharpness of the sell-off was exacerbated by the forced unwinding of Liability Driven Investment (LDI) positions, as UK pension schemes worked to provide collateral to LDI managers following sharp yield increases.

However, in Q4 2022, yields fell back across the curve following a government U-turn on fiscal policy and Liz Truss’ resignation as prime minister. Later in the period, in Q1 2023, the UK fixed-interest gilt curve fell across all maturities except for the shortest end of the curve, as markets priced in additional rate increases in the immediate future, but a lower terminal rate thereafter.

Credit markets declined over the period, with UK investment-grade credit spreads (the difference between corporate and government bond yields) widening. The iBoxx Sterling Non-Gilt index declined -10.2% as rising gilt yields and widening spreads outweighed the income yield.

Global Fixed Income

The global bonds market faced significant volatility over the period, with major central banks escalating their monetary policy tightening plans to fight inflation, and market concerns over the health of the economy resulting in intense market swings. The hawkish monetary policy resulted in a rapid rise in sovereign bond yields in June 2022, a move that was swiftly tempered as the market focus shifted to growth concerns. July’s sovereign bond rally gave way to a sharp sell-off from mid-August onwards as major central banks, led by the Federal Reserve, became more aggressive on fighting inflation, causing bond yields to rise materially. In November 2022, the US core consumer price index increased below expectation though, which raised market expectations of a change in monetary policy and resulted in a rally in the bond markets. However, major central banks continued to deliver on rate hikes, driving yields higher again from mid-December. The period’s sell-offs intensified at the end of December 2023 when the Bank of Japan unexpectedly decided to make its yield curve control policy more flexible.

Q1 2023 kicked off with a strong rally in government bond markets, driven by the prospect of easier monetary policy due to disappointing economic data. Markets swung the other way in February, with a sell-off, following strong employment and inflation data, which continued until early March when Federal Reserve policymakers reinforced their bias for higher interest rates. The failure of some US regional banks, and broader concerns about the Financials sector fuelled demand for safe-haven assets, including government debt. Prompt action by major central banks stabilised market sentiment, and as a result, global bond yields ended Q1 2023 lower, with peripheral bond yields in Europe seeing larger declines than core markets in the second half of March.

In emerging markets, a stronger dollar and weak risk environment put domestic government bonds under pressure, resulting in broad losses at the start of the period. Over Q4 2022, local emerging market government bonds were broadly supported by: bouts of US dollar weakness; the overall increase in risk sentiment given lower-than-expected US inflation; and the reopening of China’s economy. At the start of 2023, emerging markets local currency government bonds generated strong positive total returns in the first quarter, broadly supported by a weakening US dollar.

Property

UK commercial property returned -14.7% over the year as capital values depreciated, following sharply higher capitalisation rates over the year. Income return was 5.0%, but the -18.8% decrease in capital values weighed over. The retail, office, and industrials sectors fell by -7.8%, -13.2%, and -21.2% respectively.

In global property, leasing activity softened towards the end of 2022 and slowed further over the first quarter of 2023 with credit tightening in the private sector. By historical standards, multifamily and logistics leasing held up with robust rent growth and near record-low vacancies, with strong occupier demand continuing to support long-term income growth. By contrast, global office take-up fell by 23% in Q4 2022 year-on-year. Office demand fell particularly sharply in the US and rental income is expected to decrease in the foreseeable future, with potential large resets as delinquency rises in the sector.

Infrastructure

Infrastructure funds generally performed in line with their objectives over the year, although diversification across sub-sectors continued to be important for returns. While sectors such as communication and utilities experienced little or no impact from COVID, other sectors like transportation witnessed a material impact. These assets performed more strongly on the back of recovery over most of 2022 as trade and travel related volumes recovered significantly. Sea ports and terminals witnessed record headline containership volumes, however volumes normalised in the latter part of 2022 and Q1 2023. In addition, continued pick up in energy transition and the introduction of the Inflation Reduction Act in the US alongside similar policy frameworks in Europe further supported renewable energy development as well as other projects and assets critical for the energy transition.